📢 Stay Ahead of Industry Shifts with Payroll Question Time

Keep your finger on the pulse of the latest payroll changes and compliance guidelines with our insightful webinars.

Here’s your ultimate guide to payroll legislation for tax year 2024-25 and beyond! Where relevant we will provide links to official government resources for your convenience. If you have any queries along the way, remember that SD Worx are always here to help!

This guide covers information as it relates to:

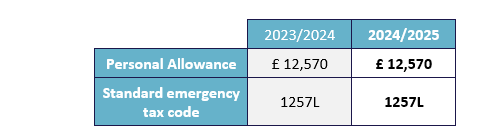

Income Tax allowances, rates and thresholds effective from 6th April 2024 for England and Northern Ireland have been confirmed as remaining frozen.

The following values are set by the United Kingdom government and are not devolved:

Those earning more than £100,000 will see their Personal Allowance reduced by £1 for every £2 earned over £100,000.

The Autumn statement 2023 announced the intention to continue to freeze the personal tax-free allowance until April 2028. The position for April 2024 has been confirmed as frozen.

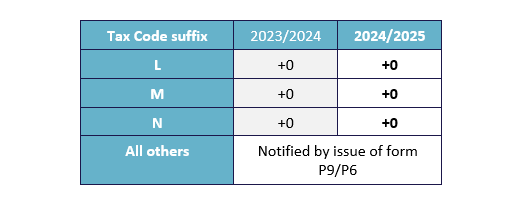

As the personal tax free amounts continues to be frozen, then there is no anticipated general tax code uplifts which are instructed by authority of form P9X

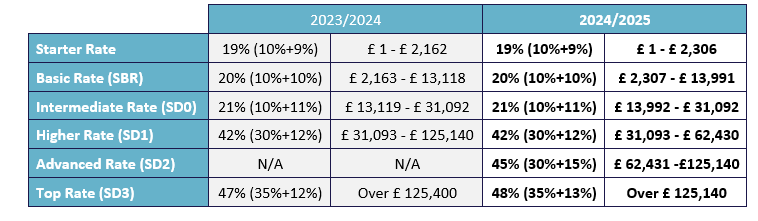

The UK Westminster government Autumn Statement 2023 has confirmed the following:

The Scottish Parliament held its Budget on 19th December 2023 and announced changes to Scottish Tax operational from 6th April 2024:

The Welsh Assembly announce on 19th December 2023 that it will retain alignment with the rest of the United Kingdom Tax (rUK) in relation to the Welsh Tax Rate for the 2024/2025 tax year and that the tax threshold and rates will remain frozen. The following is to be apply from 6th April 2024:

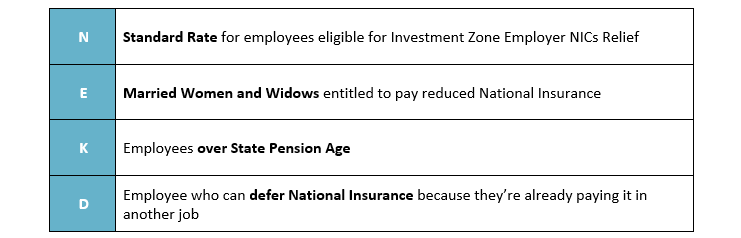

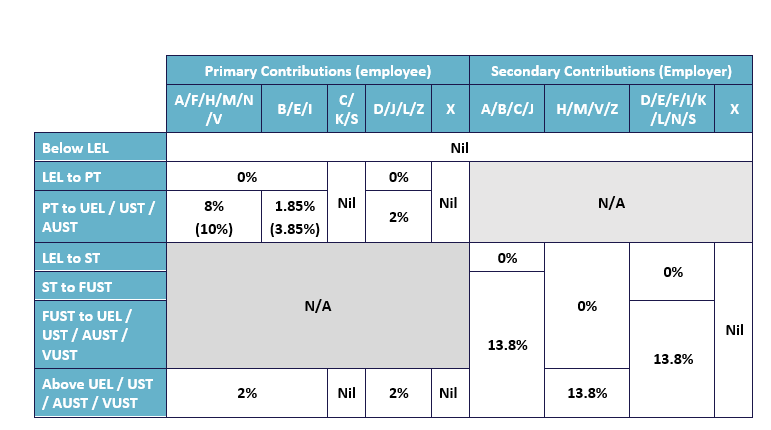

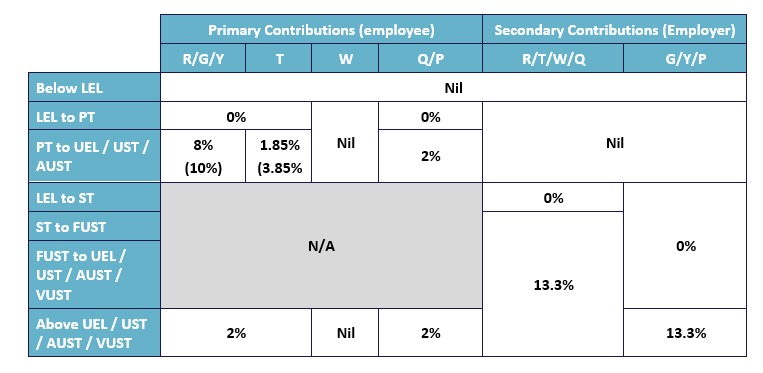

New NIC categories are introduced for use from 6th April 2024 for employers who have business premises in an Investment Zone Tax Site.

The employee must have commenced employment from 6th April 2022 and expires after 36 months of their start.

The Investment Zone Upper Secondary Threshold matches the Freeport Upper Secondary Threshold and for the Freeports and Investment Zone Upper Secondary Threshold.

Keep your finger on the pulse of the latest payroll changes and compliance guidelines with our insightful webinars.

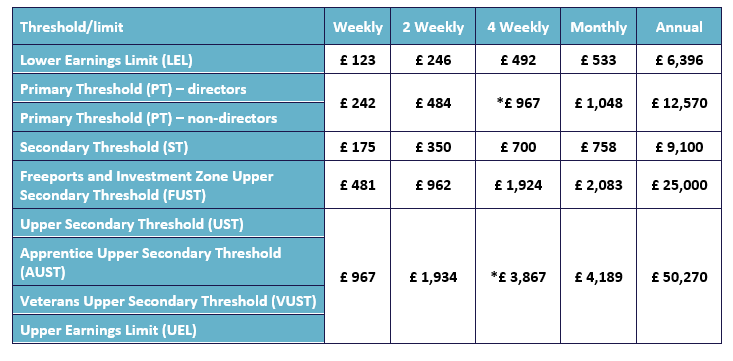

The thresholds and limits remain frozen for April 2024 with the secondary threshold being frozen until April 2028:

*Please note that due to different rounding rules in relation to Tax law versus NI law, the PT/ST/FUST/AUST/UST/VUST/UEL for 2/4 weekly is not necessarily a multiple of the weekly value. However, and for this tax year, the LEL, PT, ST, FUST are coincidently multiples of the weekly values. The UST, AUST, VUST and UEL continue to not be multiples for 4 weekly pay periods.

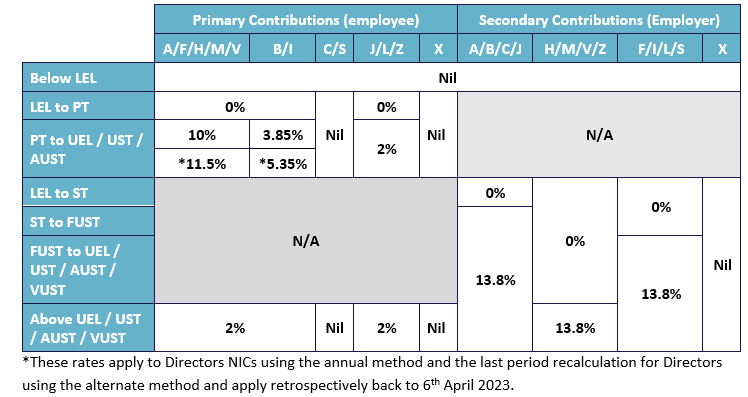

The following apply for both employees and directors from 6th January 2024:

And for Mariner related National Insurance Contributions:

For the latest insights and updates in payroll and HR subscribe to our monthly email update.

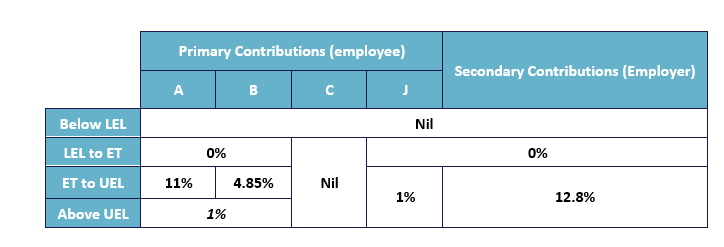

In the government budget 2024 held on 6th March 2024, the Chancellor announced a further reduction 2 percentage point reduction in the primary NIC rates.

These changes were announced late in the day and there is a potential that some payroll software or payroll processing in the early part of the new year will not have had time to update and apply the reduction. Adjustments may be required in later pay period.

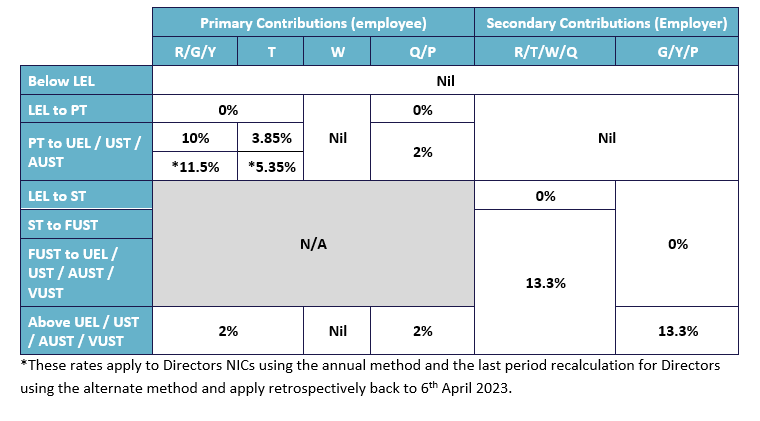

The following apply for both employees and directors (both alternate an annual method) from 6th April 2024 (with prior values shown in brackets):

And for Mariner related National Insurance Contributions:

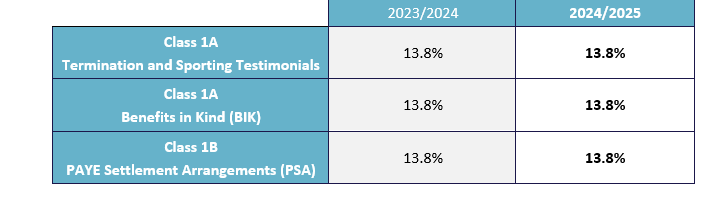

From 6th April 2024, the rates continue using the frozen standard percentages:

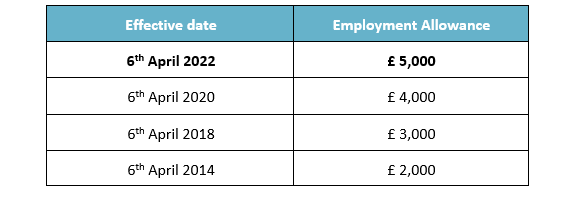

As part of the Spring Statement on 23rd March 2022, the Chancellor, Rishi Sunak, announced an increase of the employment allowance for qualifying employers from 6th April 2022. This continues for April 2024.

Family related leave

Statutory Parental Payments:

• Statutory Maternity Pay (SMP)

• Statutory Adoption Pay (SAP)

• Shared Parental Pay (ShPP)

• Statutory Paternity Pay (SPP)

• Statutory Parental Bereavement Pay (SPBP)

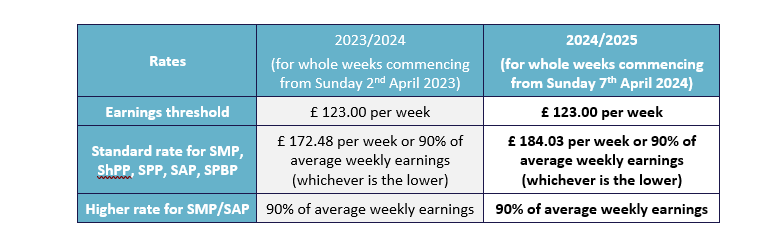

The Statutory Payment threshold and rates change have been confirmed with a 6.7% uplift for weeks of statutory payment due on or after Sunday 7th April 2023.

The Small Employers Compensation Rate remains at 3% (on payments made on or after 6th April 2011). The Small Employers Relief (SER) Threshold is £45,000.

Embrace the strategic benefits of SAP HR & Payroll integration with SD Worx's expert guidance.

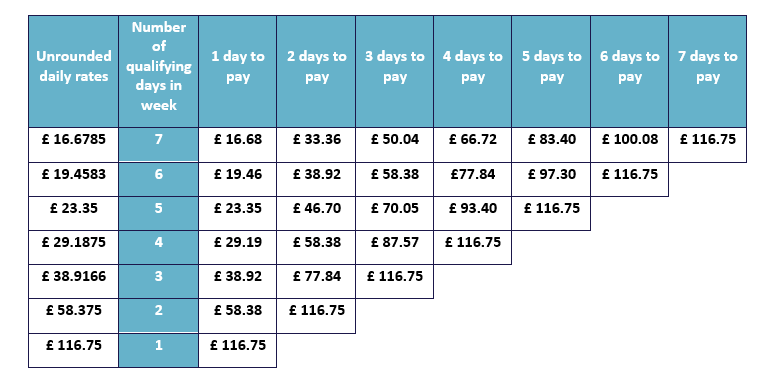

Statutory Sick Pay (changes on 6th April 2024)

The same weekly SSP rate applies to all employees. However, the amount you must pay an employee for each day they’re off work due to illness (the daily rate) depends on the number of ‘qualifying days’ they work each week.

The daily rates table have been confirmed:

The State Pension age between Males and Females are now aligned for new retirees. The gov.uk service offers tools for calculating state pension age: https://www.gov.uk/calculate-state-pension

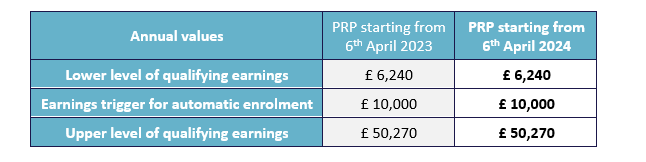

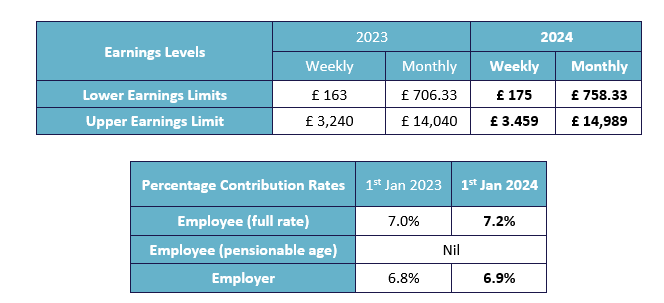

The Minister for Pensions confirmed on Tuesday 6th February 2024 the pension earnings levels and triggers for 2024/2025 in relation to ‘Pay Reference Periods’ (PRP) which start on or after 6th April 2024. They remain frozen at the same levels as April 2022:

Please note that for payments made in the new tax year where the Pay Reference Period commences prior to 6th April 2024 (such as 1st April 2024), then the 2023/2024 levels and triggers would apply. This has no impact in April 2024 as the levels and triggers remain frozen. Employers also have the option to use the tax period as the Pay Reference Period (PRP).

Further consultation will occur on the reducing of the Pension AE age and threshold for a future implementation point.

Our SD Worx Academy training centre offers courses that can help your team adapt to new systems smoothly, stay compliant and much more!

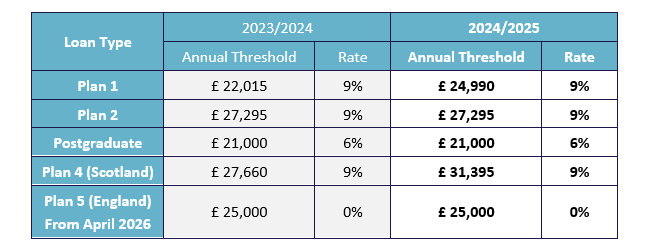

The thresholds for student and postgraduate loan borrowers are revised annually and applicable from 6th April. The thresholds are the annual amounts that can be earned before any student loan or postgraduate loan deduction is applied (on a pro-ration basis for the tax period). It is possible to have both a single student loan and postgraduate loan to be deducted at the same time.

The thresholds applicable from 6th April 2024 for Plan 1 and 2 were confirmed on Wednesday 23rd August 2023. Plan 4 confirmed on Monday 4th December 2023 and Postgraduate confirmed as frozen on Friday 2nd February 2024 (why the wait?).

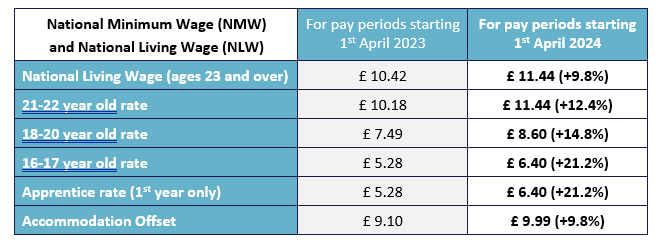

The UK government announced changes as part of the Autumn Statement 2023 announcements confirming the approval of the Low Pay Commission recommendation for the uplifting of minimum pay rates within the United Kingdom – when they do the new minimum rates apply for pay periods commencing on or after 1st April 2024.

National Minimum pay is not about the employee hourly pay rate, but about the hourly rate received after any relevant reductions, and deductions for the benefit of the employer. Important factors are the accurate recording of working time as defined by NMW law and the treatment of certain working expenses, such as ‘uniform’. Timing of work and payment is also critical. Some amounts of pay do not count towards NMW pay such as the premium element of overtime. Absence is not counted as working time. It is possible for employees with hourly pay rates above perceived minimums are actually paid below National Minimum Wage.

These increases may result in lower paid employees no longer being able to participate in salary sacrifice or salary exchange arrangements where there is not sufficient excess pay to exchange.

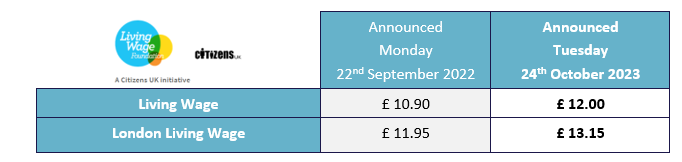

The real Living Wage is the only UK wage rate that is voluntarily paid by 9,000 UK businesses who believe their staff deserve a wage which meets every-day needs - like the weekly shop, or a surprise trip to the dentist.

The Living Wage is historically announced annually in November by the Living Wage Foundation, A Citizens UK initiative. In 2023, the announcement was made on 24th October 2023.

Living Wage employers usually have a period of six months from the announcement to implement the Living Wage within their business and retain the use of the Living Wage accreditation. This time the announcement has been made prior to the start of the Living Wage week (6-13th November 2023), however, the deadline for an accredited employer is to implement the rates by 6th May 2024.

It is still possible for an employer who pays the Living Wage to be in breach of the government National Minimum Wage laws as the basis of qualifying and payment are different. Living Wage is about the rate of pay paid, whereas the National Minimum Wage and National Living Wage are about the pay received across the amount of time worked.

Looking to change payroll providers, or starting a new payroll transformation project?

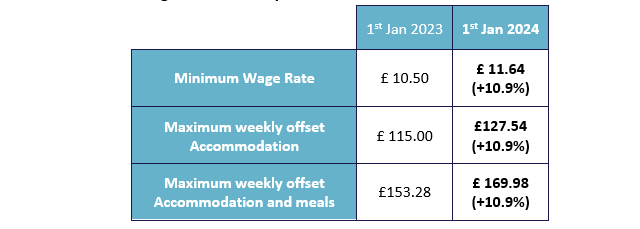

The States of Guernsey tax year commences annually on 1st January.

The States of Guernsey has approved the changes applicable from 1st January 2024:

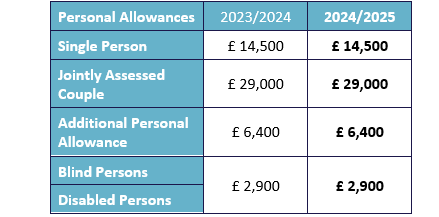

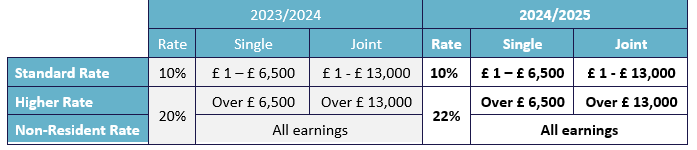

The States of Jersey tax year commences annually on 1st January.

The values to be applied from 1st January 2024 are confirmed as:

https://www.gov.je/Working/Contributions/pages/contributionlevels.aspx

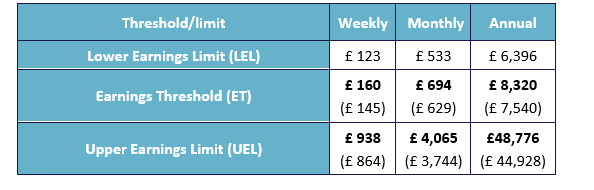

Since 1st January 2022, employers are required to pay primary and secondary Social Security contributions for any employees with wages at, or above, the minimum earnings threshold for the wage period. This replaced the former 8 hours per week trigger:

The National Minimum Wage rates for Jersey are as follows:

The Isle of Man tax year commences annually on 6th April. The values applicable from 6th April 2024 were announced on Tuesday 20th February 2024.

https://www.gov.im/categories/tax-vat-and-your-money/income-tax-and-national-insurance/budget-2024/

https://www.gov.im/media/1382355/pn-222-24-budget-2024.pdf

https://www.gov.im/media/1382356/pn-223-24-benefit-in-kind.pdf

The Isle of Man Budget 2024 has confirmed the following are frozen:

The tax rates and bands applicable from 6th April 2024 for the 2024/2025 tax year were confirmed on Tuesday 20th February 2024:

The Isle of Man confirmed on Tuesday 20th February 2024 the changes that apply from 6th April 2024 (Prior year 2023/2024 values are shown in brackets where different):

The National Insurance Contribution rates to apply for payment due from 6th April 2024 are also confirmed:

As part of the 2024 Budget, the Minister for the Treasury, the Hon. Dr Alex Allinson, MHK announced that with effect from 6th April 2024 the cash equivalent for car and fuel benefits provided by employers to employees will be calculated in accordance with the Income Tax (Benefits in Kind) (Car and Fuel) Order 2024.

See: pn-223-24-benefit-in-kind.pdf (gov.im)

Disclaimer:

The information provided does not constitute personal financial or personal taxation advice. The views expressed are the opinions of their author/compiler based on information and facts applicable at the time of publication. Some views will be expressed in relation to future legislation which may still be subject to parliamentary approval and subject to change.

Looking for more efficient payroll management? From outsourced payroll which manage the whole process for you to bespoke software built around your staff’s needs, we’ve got it all!

Join our expert panel, and hundreds of members of the Payroll & HR community, at our monthly interactive webinar.

We break down all the latest changes in legislation and field your burning questions through our live Q&A!

You’ve got a good relationship with your payroll supplier. They understand you, support you, they’re your hero and your rock at the end of every payment run. But… What if there’s something better out there? What about moving to a global payroll provider?

An exclusive relationship isn’t the only option…

With just three months to go until the General Data Protection Regulation (GDPR) comes into force, the clock is ticking for HR and payroll managers to get the systems and processes in place to ensure compliance. The regulation, coming into effect on 25 May 2018, updates data rights for today’s networked world, and organisations ignore it at their peril.